Jumbo Reverse Mortgages

The reverse mortgage has made tremendous strides since it was first introduced back in 1961.

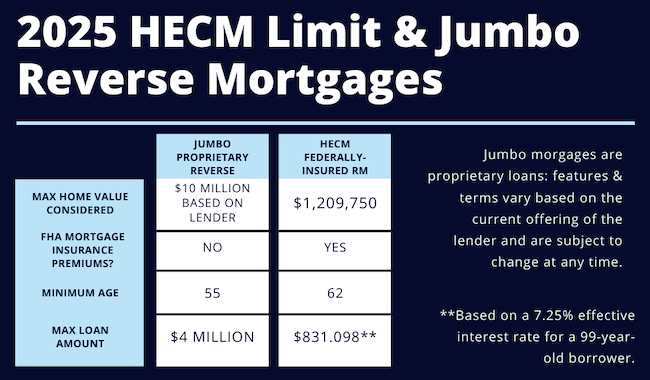

Until recently, the only reverse mortgage program available was the Home Equity Conversion Mortgage (HECM), which remains the primary type of loan used today. The only limitation of this loan, if you can call it that, is that it caps a property’s value up to the current FHA national limit. Because of this, it also caps the maximum loan amount available. While this is often sufficient for much of the country, it can sometimes fall short in areas where property values are much higher, limiting the homeowner’s access to a portion of their available equity.

Today, there are two types of reverse mortgages available: Home Equity Conversion Mortgages (insured by the FHA), commonly referred to as HECMs, and newer proprietary reverse mortgages, often called Jumbo Reverse Mortgages. You’re probably more familiar with the former, thanks to television and print ads featuring celebrities touting the benefits of a “reverse mortgage.” However, Jumbo reverse mortgages are now making a significant impact in the market, especially due to rising property values across the country.

The good news is that homeowners with higher-valued properties who want to access and use a portion of their home’s equity during retirement can now tap into much more of their home’s value—and therefore more of their equity. This can help eliminate higher loan balances and payments, if applicable, while also providing access to larger credit lines or cash-out options through a reverse mortgage.

Jumbo reverse mortgages are designed specifically for homeowners with properties that exceed the federal lending limit (currently $1,209,750 as of 2024), allowing them to access a greater portion of their home’s value. For example, if you own a $2,000,000 home, a Jumbo reverse mortgage lets you tap into its full value, rather than being limited by the HECM’s current maximum cap.

Additionally, while a traditional HECM loan requires at least one borrower to be 62 or older, the proprietary Jumbo reverse mortgage program lowers the minimum age to 55 (or 60, depending on the state). Being able to access this equity up to 7 years earlier can make a substantial difference in many ways.

Contact me today to learn more and/or for an assessment of your own unique situation.

Unique features of a Jumbo Reverse Mortgage:

While Jumbo reverse mortgages have many similarities with the traditional HECM reverse mortgage, they are unique for a number of reasons. One of the most notable and obvious differences is that a jumbo reverse loan go as high as $4 million, with property considered up to $10 million (with some lenders).

Another difference is that these proprietary mortgages do not require the significant up fron and monthly mortgage insurance premiums that are required on the traditional HECM. This means that most significant closing cost and ongoing monthly charges associated with the traditional reverse mortgage is eliminated.

Another difference: While the HECM is a government-based program, overseen by HUD, a jumbo reverse mortgage is a private, or proprietary, loan, with loan terms, conditions and guarantees that are established by the lender versus the tHECM reverse mortgage (which is administered by HUD and insured by the Federal Housing Administration).

Here are some of the features of today’s Jumbo Reverse mortgages (features and benefits may vary slightly by the issuing bank and jumbo loan product chosen):

Loan amounts to $4,000,000

Property Values to $10,000,000

No first year distribution limitations

No costly up-fron MI premium

No monthly MI premium of .50%

100% of loan funds available at closing

Would you be interested in a more detailed comparison of Jumbo and HECM reverse mortgages?

Contact me today to learn more or for a free, no-obligation assessment of your situation and needs.

Steve Kaye

Certified Reverse Mortgage Specialist for AZ and CA

NMLS #234765 | CA DRE #01118522 | AZ #LO-1038005

Arizona Corp. Branch Location 7150 E. Camelback Rd, Suite 444-430

Scottsdale, AZ 85721

Phone: Cell: (949) 350-4992

C2 Reverse Mortgage, NMLS #135622 | CA DRE #01821025 | AZ #919209